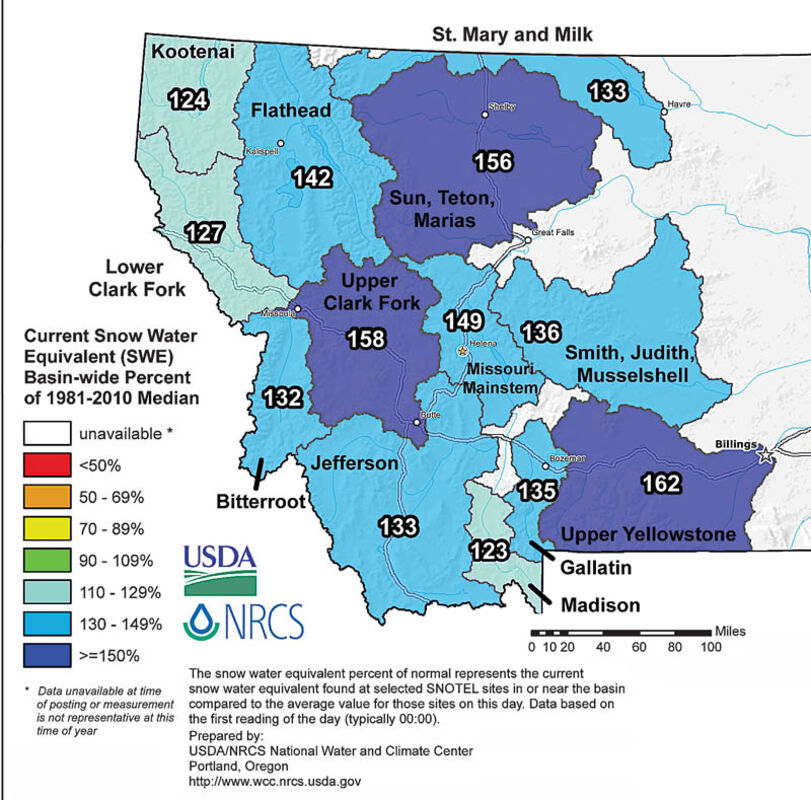

Montana SNOTEL Current Snow Water Equivalent Percent of Normal as of March 12, 2018.

When we think of floods, we have an image in our heads of cars being swept down the road or boats navigating through neighborhoods rescuing families who are seeking refuge on their rooftops. Because of these images, many people feel like they don't need flood insurance. They think that won't happen in Montana. While you may not have to wait on your roof for a boat to rescue you, floods can affect you and damage your home. Nearly 20 percent of all flood insurance claims come from moderate to low risk areas.

This year, we have an even higher likelihood of flooding for two reasons. First, the majority of Northwest Montana has 130 percent or more snow water than average. Any amount of snowmelt entering your home is considered a flood and even just one inch of flood damage in an average home can cost you up to $27,000.

Most people don't realize that snowmelt is considered flood water and you don't have to be next to a body of water to be at risk. If all the snow melts suddenly, it has a higher likelihood of entering your home because there is nowhere for the moisture to go.

Second, wildfires increase flood risk. Wildfires alter the vegetation and soil depending on the severity of the fire. In moderate and high severity fires the vegetation is killed allowing more water to run off an area since the plants are not present. In addition the soils can become hydrophobic, actually repelling water instead of absorbing it. This combination can lead to flash flooding and mudflows as we witnessed in California after their devastating fires. Flood risk remains significantly higher until vegetation is restored, which can take up to five years after a wildfire.

Most homeowners' and renters' policies do not cover flood damage so it is important for you to get a separate flood policy. FEMA requires a 30-day waiting period from date of purchase of your flood policy until it goes into effect. There are a few exceptions to the 30-day wait, the most common being that you purchase a new home and require flood coverage on the home at closing.

The 30-day wait means that if you purchase flood insurance and a flood occurs within that 30 day window, there will be no coverage. For example, if you had a flood 20 days after you purchased the flood policy, there would be no coverage.

The flood insurance premium is based on the flood zone your home is in, occupancy, the value of your home and if you have had prior flood losses among other factors. As the snow starts to melt, it is a good time to contact your insurance agent to get an estimate. Remember, you will have to wait 30 days until your flood insurance is in effect.

If you have questions please don't hesitate to call your local insurance agent.

*Statistics and figures from http://www.fema.gov and USDA.

Reader Comments(0)